ETS 2012-2020

From 2012 to 2020, all flights to and from an airport in the European Economic Area (EEA) were supposed to be covered by the ETS (‘full scope’). However, it was changed to only cover intra-EEA flights until the end of 2023 [5]. This ‘stop the clock’ measure was due to international pressure, with the understanding that the International Civil Aviation Organisation would in the meantime develop an international mechanism [6].

There are specific allowances for aviation in the ETS known as EU Aviation Allowances (EUAAs), but airlines can also buy the general EU Allowances (EUAs) for stationary installations [6]. The cap on EUAAs was defined as some percentage of 2004-2006 emissions levels: 97% for 2012 and 95% thereafter [7, 8]. 82% was allocated for free based on efficiency. 15% was auctioned and the remaining 3% was put in a special reserve for fast-growing aircraft operators and new entrants [7].

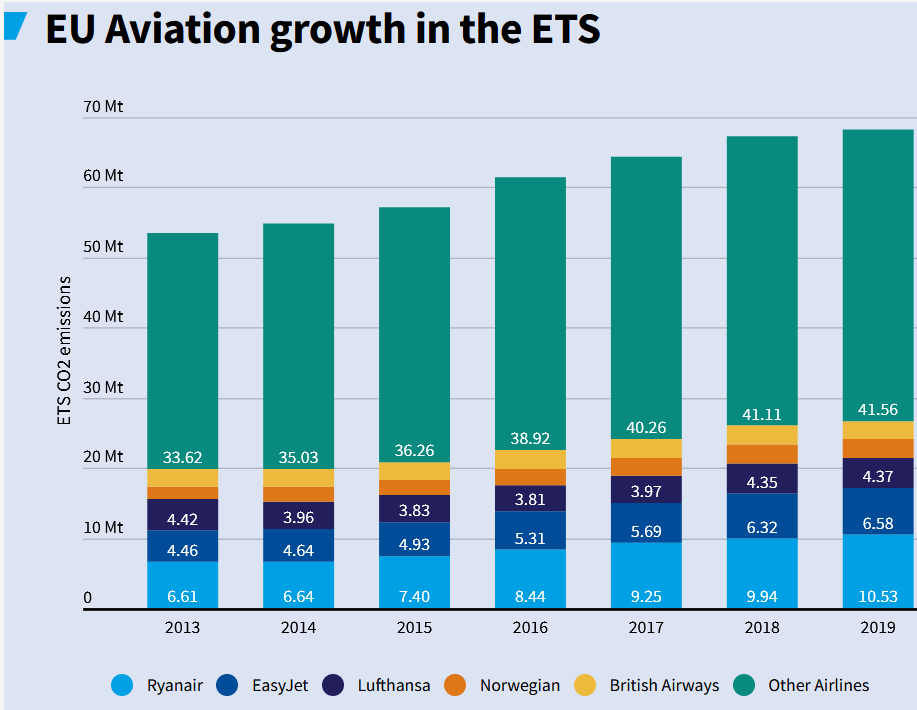

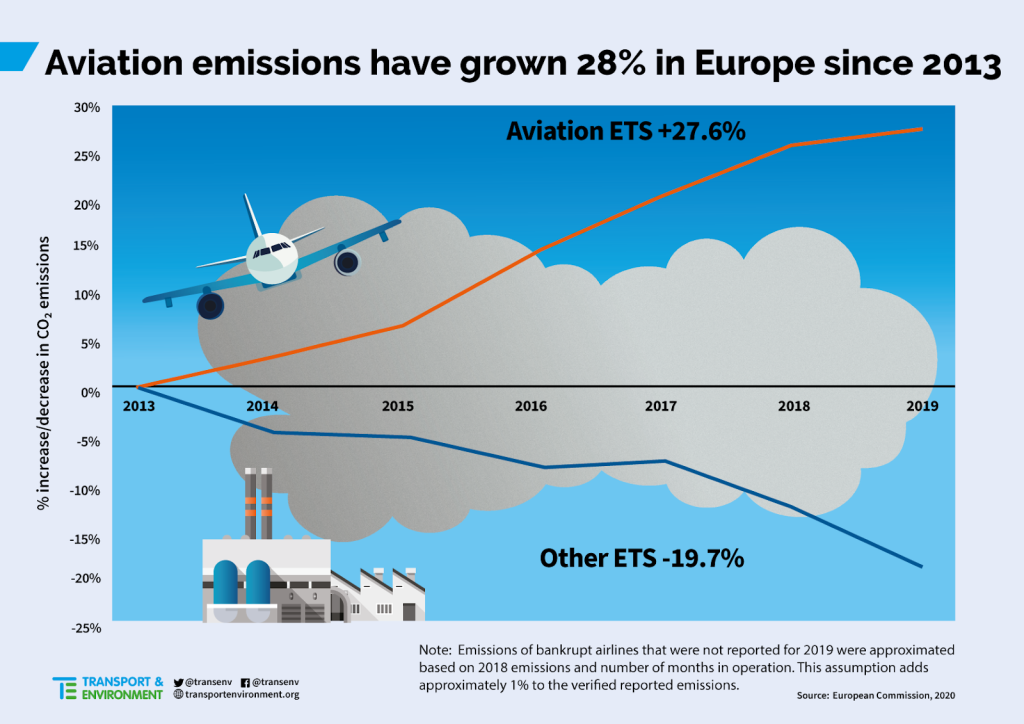

In 2019, aviation emissions increased by 1.5% in the ETS compared to a 8.9% decrease for other sectors. Figure 1 shows the annual emissions for aviation under the ETS. Ryanair on its own was the 7th largest emitter in all of the ETS (stationary + aviation) in 2019. Overall, aviation emissions under the ETS have increased by 27.6% between 2013 and 2019 (Figure 2). This is in contrast with the rest of the ETS which saw a decline by 19.7% [9].

Figure 1. Annual ETS emissions for aviation per airline [9].

Figure 2. Evolution of emissions under the ETS of aviation vs non-aviation [9].

How the auctioning revenue was used, was up to the Member states. The Directive only stated that revenue “should” be used for climate action in the EU and outside [8].

ETS 2021-2031

As part of the fit for 55 package, rules for aviation in the ETS are being revised [10]. Under the proposal, free allocation will be reduced by 25% annually starting from 2024, reaching full auctioning in 2027 [11]. In the recent report by the rapporteur, she proposes to accelerate the phase out and reach full auctioning in 2026 [12]. Currently, a linear reduction factor of 2.2% will be applied from 2021 to the cap [13]. But under the proposal, this would change in 2024 [11]. The cap for 2024 is defined as the number of allowances in 2023 reduced by a linear reduction factor of 4.2% and the linear reduction factor would continue to be 4.2% in the following years [11, 14].

Regarding revenue use, “Member States shall use the revenues generated from the auctioning of allowances in accordance with Article 10(3)” [11]. Article 10(3) refers to the ETS Directive and is itself being revised from requiring at least 50% of auction revenue going to climate action, to 100% [15, 16]. In reports from the European Parliament, some earmarking of funding to decarbonizing aviation is proposed, either from the Innovation Fund or directly from auctioning revenue [12, 17].

The scope would continue to cover intra-EEA flights but also flights to the UK and Switzerland. For other international flights, the EU would apply CORSIA [18].

CORSIA

The Carbon Offsetting and Reduction Scheme for International Aviation (CORSIA) is a global market-based mechanism created to tackle CO2 emissions from international aviation. Central to it is the goal of stabilising international civil aviation net CO2 emissions at 2019 levels through offsetting. Offsetting refers to financing emission reductions elsewhere to compensate for your own emissions [19]. Airlines operating routes between participating states will have to buy offsets to compensate for increased emissions compared to the baseline [20]. There are three phases of CORSIA:

- Voluntary pilot phase from 2021-2023

- Voluntary first phase from 2024-2026

- Mandatory second phase between 2027-2035 [21]

However, this scheme has several flaws:

- the quality of offsets is often questionable;

- the switch in baseline from 2020 to 2019 and reduced aviation activity due to Covid-19, make it more likely that demand for offset credits in CORSIA’s pilot phase will be zero [22];

- Key markets such as China, Russia and India remain out of the voluntary phases [22, 23];

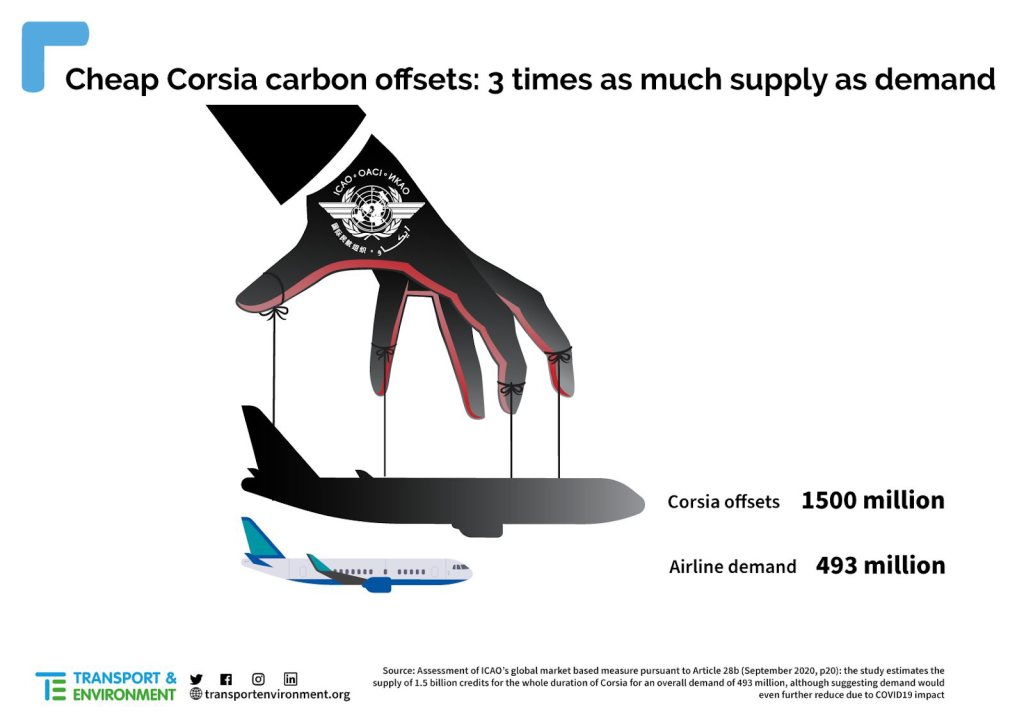

- there will be an oversupply of cheap offset credits meaning no incentives to actually reduce emissions (Figure 4);

- there is a lack of transparency as countries do not have to publish offsetting requirements of their airline operators. This makes it impossible to monitor whether countries are really implementing CORSIA [22]. In the recent report by the rapporteur, she proposes to correct this and have the data public [12].

Figure 3. CORSIA will provide much more offsets than the sector actually needs [20].

Conclusion

Aviation emissions have significantly increased despite being included in the EU’s Emissions Trading System. The transition to full auctioning and introduction of a linear reduction factor are welcome changes. Together with changes in the Energy Taxation Directive, the new ReFuelEU Aviation Initiative and other legislation, this will help the decarbonization of the aviation sector in the EU. Whether it will be achieved, remains to be seen. But it is clear that the EU cannot wait for the rest of the world to take action.